San Diego Housing

commentary

Search

Our Housing Research

Our Housing Seminars

Sign up for our newsletter

More stuff

Media

Guest Column

In the News

Answers

Housing Basics

Alternatives to Foreclosure

Real Estate Investing

Tenant Rights

Books

Disclaimer

Our Mission

The HOA Trap: Think Twice Before Buying Condominium or Townhome

Most people are attracted to the lower price of a townhouse or condominium home. There can be savings of up to 30-40%. Some are pretty good deals. I’ve seen 3 bedroom town homes of 1500 – 1700 square feet for two thirds of a single family dwelling. Many are very spacious with nice features.

At first glance it looks like a pretty good deal. Some homes look like a single family dwelling on the inside with one common wall. What many buyers don’t realize is the high cost and hassle of the Home Owner Association (HOA). A bad HOA can make your life miserable.

In general the HOA is an organization that covers the exterior maintenance of your home and other units in the complex. The HOA usually covers insurance (for the exterior), landscape maintenance, repairs such as painting, concrete repair, pool service, park service etc. Each home owner in the complex pays a monthly HOA fee which is not tax deductible. This monthly fee can be expensive.

The HOA monthly fee is in addition to the cost of the mortgage, property taxes and home owner’s insurance. It’s quite common to have HOA monthly fees as high as $300 – $400 a month. If you have a $2000 a month mortgage, $200 a month property taxes, $50 a month home owner’s insurance and $300 HOA fee that adds up to a total of $2550.

Most HOAs have a governing board elected by the home owners in the condominium or town home complex. The ‘board’ usually has a president, secretary and treasurer plus additional board members. The board can act like a small governing body. Depending on the HOA bi-laws, the board decides what maintenance, repairs and enhancements should be done to the complex. The board sets priorities and HOA fees. Buy a majority vote on most HOA boards they can decide to increase HOA fees or impose special assessments to each home owner. A well run board will issue monthly income and expense statements to each home owner.

Taking in monthly HOA fees can be big business. For example if there are 100 homes in a complex and each home owner pays $300 a month that’s a total of $30,000 a month or revenue or $360,000 a year. That’s a lot of money.

There have been many cases of mismanagement and even fraud in HOAs. I know a case where the board decided each unit in the complex needed repainting. The board got a no competition bid from a painter and imposed a special assessment of $5000 on each home owner. After a contentious board meetings and investigation it was found the owner of the painting company was a friend of the board president. Competitive bids later showed each unit could be painted for $2000 each.

In another case, the board imposed a special assessment of $24,000 on each home owner in a 186 unit complex to do drainage repairs. If the home owner refused then a lien was taken against the home. Those who couldn’t pay a lump sum could arrange for a load with additional monthly payments of $250 for 15 years.

In many cases HOA boards set priorities and determine that repairs or enhancements are urgent. To the contrary, many times repairs can be done over time and in many other cases not needed at all. The home owner doesn’t have a say.

One might think a home owner can sue the HOA board but in reality he’s just suing himself because he is part of the association. A lot of power is given to HOAs.

A single family dwelling may be 30% more expensive but the home owner doesn’t have the hassle of an HOA board and all that goes with it. The single family home owner can set the urgency of repairs the priorities and eliminate high HOA fees.

Buyer beware, investigate the HOA thoroughly before buying a condominium or town home.

Search San Diego homes for sale

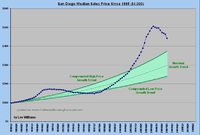

How low in Oxnard

How low in San Diego?

Lee sent me this graph today, noting that he would do this for other cities, if requested by readers.

Bruce can post these California cities

Guest Column – Automated Underwriting System

By Roger Herrick

One of the major changes that has occurred in the mortgage lending industry during the past few years is the utilization of computers to underwrite mortgage loans. Hence the name – automated underwriting. The benefits of automated underwriting is significant – faster loan approvals, reduced closing costs, less documentation requirements, and the approval of many loan applications that in the past were denied. As these systems become more accepted by lenders and secondary markets more loans will be approved and funded.

From a lenders standpoint, instead of documenting the file first, then sending it in for an Underwriters approval, the complete application is entered into a program. Then it connects to a Fannie Mae or Freddie Mac for application submission. Within a few moments you have a complete loan approval. Simply do what the approval from Fannie or Freddie requires and your loan will be funded and the lender has a sellable loan.

Sometimes old habits die hard and clash with new technology, specifically, outdated underwriting habits.

For many years home mortgages were approved by human beings. These people were called underwriters. When people needed a home loan they would fill out a large amount of paperwork. When the paperwork was completed, they then had to document the loan. Documentation was standard from one lender to the next, and it typically included two most recent pay stubs, two most recent W2s or two most recent Tax Returns, all schedules, if self- employed. If a person wasn’t self-employed, but got more than ¼ of their income from commissions or bonuses they would not only have to provide two years tax returns, all schedules, but also a letter from their employer explaining how the employer handles employee business expenses. Also, they had to provide three months bank and investment statements. This would be only the beginning.

More paperwork would be needed after the credit report was run. But technology changed all that. Instead of documenting everything you can imagine, the consumer needs only to provide the items Fannie or Freddie Mac asked for upon an automated approval certificate. Whichever AUS was used, the exact documentation requirements are clearly spelled out. Sometimes though, your underwriter asks for more than is required. Why, because they can and sometimes those requests are reasonable.

If an AUS asks for only one pay stub then why would an underwriter ask for two pay stubs and last years W2? Old habits die hard. During the old days it was automatic to ask for pay stubs and W2s. But if the AUS doesn’t ask for it, it’s not needed. This happens many times, most often when someone’s self-employed. Getting the first two pages of last year’s tax returns is a lot less than two years, full schedules plus a year-to-date P&L. Underwriters aren’t trying to make themselves work any harder, they have requested it so many times in the past and automatically ask for it. Old habits are hard to break.

—

Roger W. Herrick

Mortgage Professional

1201 Puerta Del Sol Suite 201

San Clemente, CA 92673

Direct (888) 619-9044

Fax (714) 464-4287

Email [email protected]

Website www.ContactHerrick.com

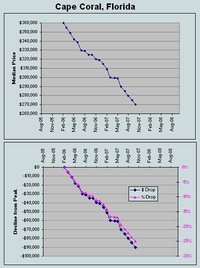

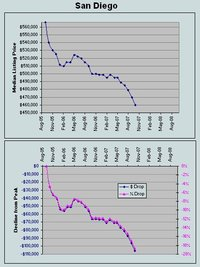

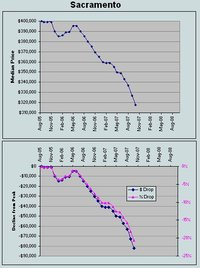

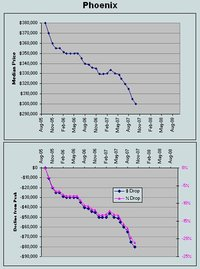

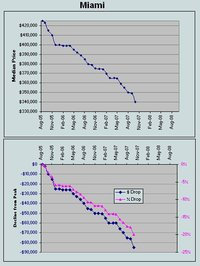

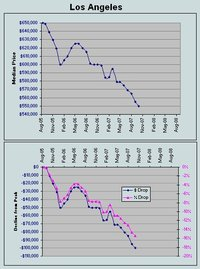

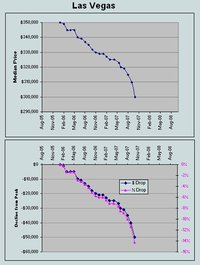

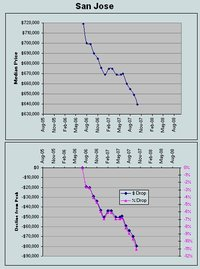

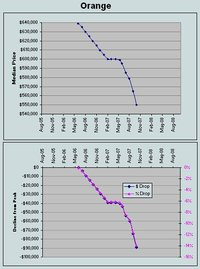

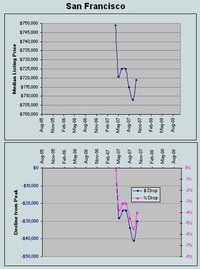

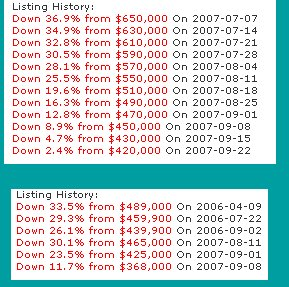

Median Listing Prices for October

Below are graphs of the Median Listing Prices for various cities in the US updated through October 1, 2007. The charts are “peak to present”. The data comes from HousingTracker .

Listing prices foreshadow sales prices; they are 3-4 months ahead of sales. There was a brief discussion of Sales Prices vs. Listing Prices here if you have not seen it.

Click to enlarge of course…

— Lee Williams

San Diego Info